Two major climate disasters have gripped the nation in recent months. In January, four separate wildfires driven by 100 mph Santa Ana winds destroyed cities and towns in Southern California, including Pacific Palisades, Malibu, Altadena, and Pasadena. At least 10,000 structures, including entire residential neighborhoods, were leveled. Over 100,000 people were ordered to evacuate, and at least 16 are dead.

Last fall, Hurricane Helene made landfall in Florida as a Category 4 storm, but quickly worked its way inland. Most impacted was Western North Carolina, the mountainous region of Asheville, previously thought to be a climate haven. Storm surges, landslides, and power outages washed way and cut off entire communities. At least 230 people died. Hurricane Milton followed two weeks later, hitting already damaged coastal Florida. Months later, the trauma still lingers for everyone in the disaster zone.

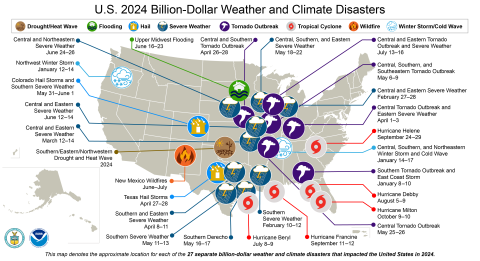

Unprecedented is a word often used to describe these extreme climate events. Yet such events are becoming increasingly common. The year 2024 saw 27 climate disasters costing $1 billion or more, the second-most on record (2023 had 28). Last year was also the warmest year on record, and the first time the Earth passed 1.5°C of warming since pre-industrial times.

At the center of these disasters is property insurance. Anytime someone’s home or business is damaged or destroyed in a fire or storm, they expect their insurance to foot the bill to recover and rebuild. Yet in Southern California, thousands of homeowners were dropped by State Farm a few months before the fires, and in Western North Carolina, almost no one had flood insurance.

Insurance at a crossroads

Property insurance has reached a crisis point – but in crisis is also opportunity. In their roles as both insurance providers in case of disaster and major institutional investors, big insurance companies have the unique power to determine what our future looks like.

These companies could continue business as usual – a vicious cycle of insuring fossil fuel projects and investing in fossil fuel companies to make a quick profit, all while dropping policy holders in climate-vulnerable areas and raising rates on the rest of us.

Or these companies could begin a virtuous cycle of phasing out insurance and investments for fossil fuel projects and companies that make the climate crisis worse, choosing instead to use their record profits for underwriting and investing in the clean energy transition.

The first choice leads to an uninsurable future that permanently undermines the entire economy. The second choice leads to an insured future that lays the foundation for sustainable prosperity.

As a Senate Budget Committee report from December 2024 put it:

One thing is certain: unless the United States and the world rapidly transition to clean energy, climate-related extreme weather events will become both more frequent and more violent, resulting in ever-scarcer insurance and ever-higher premiums. This is predicted to cascade into plunging property values in communities where insurance becomes impossible to find or prohibitively expensive — a collapse in property values with the potential to trigger a full-scale financial crisis similar to what occurred in 2008. To avoid such a devastating fate, we must speed the transition to clean energy and eliminate carbon pollution. Climate change is no longer just an environmental problem. It is a looming economic threat.

Senate Banking Committee, Next to Fall: The Climate-Driven Insurance Crisis is Here -- and Getting Worse

Insuring our future

In its eighth annual scorecard and report, Insure Our Future -- a campaign comprised of environmental, consumer protection, and grassroots organizations holding the U.S. insurance industry accountable for its role in the climate crisis -- explores the relationship between climate change and property insurance companies worldwide.

The report, Within Our Power, has five eye-opening findings:

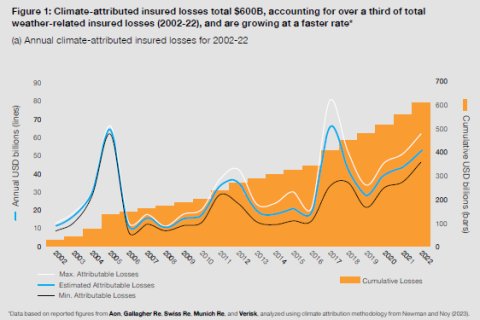

- Over one-third of weather-related losses in the past two decades – a total of $600 billion -- can be attributed to climate change. That’s an average of $30 billion per year.

- Climate-attributed losses account for a growing share of insured weather losses, showing that decarbonization is crucial to contain soaring insurance costs. Climate-attributed losses are now 38% of insurance payouts, $52 billion of $132 billion in 2022, and growing at 6.5% per year.

- Climate-attributed losses for 28 top property and casualty insurers totaled $10.6 billion in 2023 – almost equaling the $11.3 billion they took in premiums to insure fossil fuel projects. For more than half of companies, climate-related insurance payouts exceeded fossil fuel premiums. Yet revenue from fossil fuel premiums represents only 2% of their business.

- Insurance premiums for the renewable energy market was less than 30% of the fossil fuel insurance market in 2023, pointing to a bottleneck for up to $10 trillion in clean energy investments. US insurance companies especially lag in the proportion of insurance for fossil fuels over renewable energy.

- At the brink of 1.5°C, insurers are abandoning at-risk communities worldwide while enabling fossil fuel expansion that drives these risks higher – requiring immediate policy and regulatory action. Last year the Italian insurer Generali broke the cycle by ruling out oil and gas expansion, including LNG terminals.

Policy prescriptions

Insure Our Future, as well as Ceres and Climate & Community Institute, have all issued reports outlining policies that could put the property insurance industry on a more sustainable path.

Insure Our Future’s Within Our Power report calls for integrating climate risks into the regulatory framework for insurance companies, overseeing insurers’ management of climate risks, allocating climate risks and costs to protect individuals and communities, mandating data transparency, using scientific climate scenario analysis, and requiring insurers to pay more for insuring and investing in fossil fuels.

Ceres' 10-Point Plan for the Insurance Industry calls for mandatory risk disclosure, predictive climate modeling, innovative insurance products, incentivizing climate mitigation, climate-adjusted pricing models, federal climate reinsurance, mandatory and transparent climate transition, climate-resilient building codes, equity and accessibility, and leveraging insurers’ investments.

Climate & Community Institute’s Shared Fates report views the insurance crisis as a housing justice issue, calling for the creation of federal and state Housing Resilience Agencies that would provide public disaster insurance, disaster risk reduction, address renters and mobile homes, and create climate advisory councils.

What can you do?

As an individual facing this insurance crisis, here are several things you can do:

- Share this blog post with your friends!

- Learn about how the largest insurance companies are insuring risky fossil fuel projects and investing in fossil fuel companies – and which ones invest the most.

- Use Green America’s Climate Smart Insurance Directory to find insurance companies in every state that do not insure fossil fuel projects and invest little to nothing in the fossil fuel industry.

- Find out how to shop for insurance by contacting several independent insurance agents in your local area, region or state.

- Tell over 70 executives at the nation’s largest insurance companies to stop profiting off fossil fuels while leaving customers holding the climate crisis bag.

- Check out Green America’s webinar on Responsible Home and Auto Insurance, with speakers from GreenFaith, Third Act, and Insure Our Future.

- Has your insurance premium skyrocketed in recent years, or have you lost your insurance? Call the Insurance Commissioner in your state to tell your story.